Payment Orchestration Platform Costs: How Insurance Claim Transaction Methods Compare

Most insurers already know paper cheques are expensive. What catches many claims teams

off guard is how wide the cost gap has become between traditional payouts and newer.

And it’s no longer a small efficiency issue.

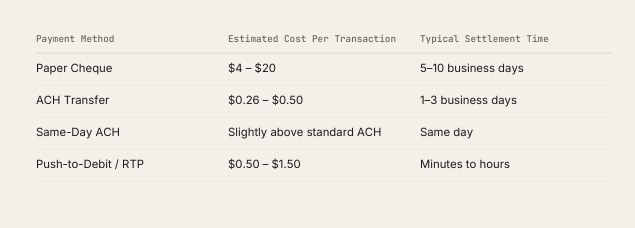

A single paper cheque can cost anywhere from $4 to $20 once printing, mailing, reconciliation work, reissues, and manual handling are included. ACH payments, meanwhile, often cost well below a dollar.

Across a few hundred payments, that difference is manageable. Across tens of thousands of claims, it starts changing operational decisions.

That’s one reason insurers have been paying much closer attention to payment orchestration platforms over the last few years. The challenge is no longer just “going digital.” It’s figuring out which payment method makes sense for which claimant – without turning claims disbursement into a fragmented operational mess.

DisburseCloud operates in exactly that space, helping insurers manage multiple payout rails through a single orchestration layer.

The Real Cost Difference Between Payment Methods

Transaction fees only tell part of the story. The bigger expense often shows up later in operations teams, reconciliation workflows, support queues, and exception handling.

Here’s how common insurance payout methods generally compare:

Research from AFP, Bottomline Technologies, Nacha, and Datos Insights continues to show the same pattern: paper remains the most expensive payment method insurers still use at scale. Even so, many carriers still depend on it heavily.

Not because they want to.

Why Paper Cheques Still Exist in Insurance

From the outside, continuing to mail cheques feels outdated. Internally, it’s more complicated than that.

A lot of claims infrastructure was built long before real-time payments became realistic. In many organizations, cheque workflows are deeply tied into legacy systems, approval processes, and accounting controls that nobody wants to rebuild casually.

There’s also the human side of it.

Some claimants still prefer physical cheques. Others don’t fully trust digital payouts, especially in large settlement situations. And in certain complex claims environments, manual review steps still fit more naturally with traditional payment handling.

So, insurers end up operating in a mixed environment:

- — ACH for routine payouts

- — Faster rails for urgent situations

- — Cheques for exceptions and claimant preference

That flexibility matters more than people assume.

Trying to force every payment through a single method usually creates new problems somewhere else in the workflow.

Where Digital Disbursements Actually Save Money

The operational savings are usually bigger.

Electronic payments reduce:

- — Cheque reissues

- — Stop-payment requests

- — Reconciliation workload

- — Fraud exposure tied to paper instruments

- — Unclaimed property risk

- — Inbound payment-status calls

That last one matters.

Claims teams sometimes underestimate how expensive payment uncertainty becomes once customers start calling support lines repeatedly asking where the money is.

For a mid-sized insurer handling high claim volume, even small reductions in support traffic can translate into meaningful operational savings over time.

McKinsey and Deloitte have both published research showing insurers can reduce payment processing overhead substantially after shifting toward digital disbursement models.

But most insurers are not trying to eliminate cheques completely.

Usually, the goal is optimization.

Route low-urgency payments through ACH. Use faster rails where speed genuinely matters.

Keep cheques available when needed. Reduce friction where possible.

That’s typically where orchestration platforms start becoming operationally useful rather than just technically interesting.

What a Payment Orchestration Platform Actually Does

At a basic level, a payment orchestration platform sits between the insurer’s claims system and multiple payout networks.

Instead of maintaining separate integrations for:

- — ACH processors

- — RTP rails

- — Card networks

- — Digital wallets

- — Cheque vendors

the insurer connects once through a centralized layer.

That sounds simple on paper. In practice, it removes a surprising amount of operational overhead.

Especially for IT teams already managing aging claims infrastructure.

It Simplifies Payment Integrations

Adding new payout methods traditionally means engineering work, testing, compliance reviews, vendor coordination, and long implementation cycles.

Orchestration platforms reduce much of that complexity by consolidating payment connectivity into one environment.

That becomes increasingly useful as newer payment rails like FedNow continue entering the market.

It Allows Dynamic Payment Routing

Not every claim needs instant payment.

In many situations, standard ACH remains the most sensible option from a cost perspective.

But there are moments where speed matters:

- — Emergency housing reimbursements

- — Catastrophe response claims

- — Total-loss auto settlements

- — Escalated customer situations

In those cases, real-time payouts may reduce operational friction more than they increase transaction cost.

That calculation is becoming more common inside claims departments.

It Helps Insurers Adapt to Changing Expectations

Consumers increasingly expect money to move quickly. They experience instant transfers elsewhere in their financial lives, so waiting over a week for a claim cheque now feels unusually slow.

Claims satisfaction data has been reflecting that shift for years.

The payment itself becomes part of the customer experience – not just the administrative final step.

Faster Payments Reduce More Than Frustration

A delayed payment rarely stays isolated as a payment issue.

It usually becomes:

- — A support issue

- — A communication issue

- — A satisfaction issue

When claimants don’t know where their payment is, they call.

And contact-center costs add up fast.

Avoiding a single extra support interaction can sometimes offset the entire premium associated with a real-time payment method.

That’s why many claims’ teams now evaluate payment speed differently than they did a few years ago.

What Insurers Should Look for in a Multi Payment Modality Platform

Not every orchestration platform is designed around insurance workflows specifically.

Claims organizations evaluating providers typically look for:

- — ACH support

- — RTP and Fednow compatibility

- — Push-to-debit capabilities

- — Digital wallet support

- — Cheque fallback handling

- — Payment tracking visibility

- — Routing controls

- — Compliance support

Implementation flexibility matters too.

Most insurers are not interested in replacing their entire claims system simply to modernize disbursements. They want something that fits around existing infrastructure without creating a multi-year migration project.

That’s largely why orchestration layers have gained traction inside insurance in the first place.

FAQs

Why do insurers still send paper cheques?

Mostly because legacy workflows still depend on them. Some claimants also continue preferring physical payments, particularly in larger or more sensitive claim situations.

Is ACH always the best option for insurance payouts?

From a pure cost perspective, usually yes. But faster rails can make more sense in situations where payment delays create support escalations or poor claimant experience.

Do orchestration platforms replace existing claims systems?

Actually, no. Most sit alongside existing infrastructure and connect through APIs, which allows insurers to modernize payments without rebuilding their entire claims environment.

Are insurers trying to eliminate cheques completely?

Usually not. Most carriers are moving toward a mixed payment environment where digital rails handle the majority of payouts while cheques remain available for exceptions.

What is the biggest operational advantage of payment orchestration?

Flexibility. Claims teams can route payments based on urgency, cost, claimant preference, and operational context without maintaining separate workflows for every payout method.